The financial cycle has ended up in a very deep financial crisis. Very low interest rates, ultra-low, even negative, policy rates epitomize this crisis; they have raised concerns about the global economy and have triggered heated debates among economists, decision-makers. Central banks, especially those which set the tone in financial markets are under scrutiny taking the center-stage of debates. Top ECB officials cite structural conditions in the European and the world economy as an explanation for the very low interest rates. In essence, these conditions refer to the balance between investment and saving[1]. The IMF also got involved in the debate by saying that ultra-low rates (even negative) are not unjustified in the current context[2]. The BIS, instead, warns repeatedly about side-effects of non-standard measures.

The natural/neutral, equilibrium rate

Demographic and productivity trends, globalization, the financial crisis, overburdening debts, income distribution, new technologies, growing uncertainties, all these have impacted strongly on investment and saving. More specifically,

- increased saving relates to demographics, income distribution, uncertain revenues, etc.

- the crisis has dented investment appetite, a natural reaction if one considers exuberance and bad investment choices in pre-crisis years; heightened uncertainties are reducing overall risk appetite --as Hyman Minsky remarked in his interpreation of Keynes, uncertainty is fundamental for understanding economic cycles[3];

- over-indebtedness (‘debt overhang’) generates a slowdown of economic activity, a balance-sheet recession (via deleveraging) as Richard Koo noticed for Japan ever since the early 1990s;

- productivity growth diminished in the US as well as in other economies over the past decades, which made Robert Gordon, Lawrence Summers and others to suggest that we have, quite likely, entered a period of lasting stagnation (secular stagnation, as Alvin Hansen put it back in 1938). Such an assumption may seem strange if it is juxtaposed to the thesis of an incoming new Industrial Revolution, but it is not without plausibility when new technologies are likely to eliminate more than create jobs;

- decreasing inflation after large emerging economies entered global competition; an import of disinflation has occurred, from China in particular. The financial and economic crisis was a shock in itself, that combined effects on both supply and demand sides. The decline in commodity prices (i.e. oil) speeded the fall of inflation.

The factors mentioned above suggest that the equilibrium interest rate, at which there is full resource utilization, has fallen significantly in industrial economies. This is also seen in the trends of long-term real interest rates and yields on 10-year bonds ( BIS data, King and Low, 2014; Rachel and Smith, 2015). In the context of a chronic under-use of resources, with intense hysteresis taking place (depreciation of idle capacities, of human capital), real policy rates would need to turn negative. If inflation is very low (even negative), central banks would be forced to take policy rates below zero (hitting the zero-bound). [4] Finally, the financial and economic crisis, the decline in economic activity and potential GDP, fuel governments’ propensity for intervening in a drive to prop-up their economies. As a matter of fact, there is a worldwide competition via competitive devaluation.

If monetary aspects are disregarded, the natural, equilibrium interest rate --according to Knut Wicksel’s definition -- balances investment and saving at full utilization of resources. The natural interest rate reflects the trade-off between current consumption versus future consumption. As the interest rate goes up, the cost of postponing spending becomes more tempting. As regards investment, a higher interest rates (credit cost) reduces its volume. The movement along the two curves reveals the dependency of saving and investment on the interest rate level; shifts of these curves indicate a change in the propensity for saving, for investment. During a major crisis both preferences might change substantially. The level of investment influences potential GDP. Such a thesis is valid provided good resource allocation takes place. If too many investments are misguided, the seeds of a crisis are sown. The natural interest rate depends on the propensity to invest and save. If the appetite for saving is on the rise, due to, say demographic trends and/or uncertainties, there is a fall of the equilibrium interest rate. In such a case, for the same returns on their capital, companies are inclined to save more. In other words, at a higher volume of saving the equilibrium interest rate edges down, more investments could therefore be financed at its level and this might push up future output. But the structure and quality of investment remain key, given their effects on the potential GDP.

The preference of households/consumers, of companies, for investment may change due to circumstances. Therefore, the investment curve may shift sideways, with the appetite for investment on the rise, or on the wane. For example, fear of what the future may bring weakens investment propensity as long as expected returns stay the same. A more unfavorable economic, social, political or geopolitical environment, as well as various uncertainties as we see now in many economies, are to be included here. And a lower cost of machinery and equipment will diminish investment volume at constant interest rates. When both curves drift sideways, the interest rate deemed appropriate for potential output would fall considerably, even below zero.

Monetary policy in a depressed economy

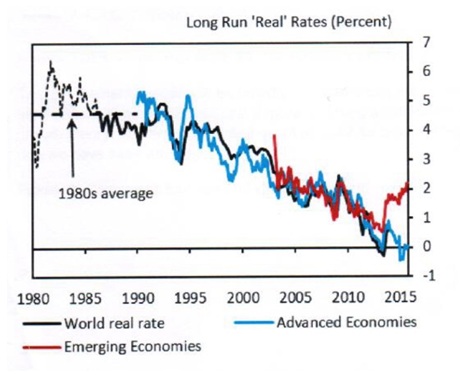

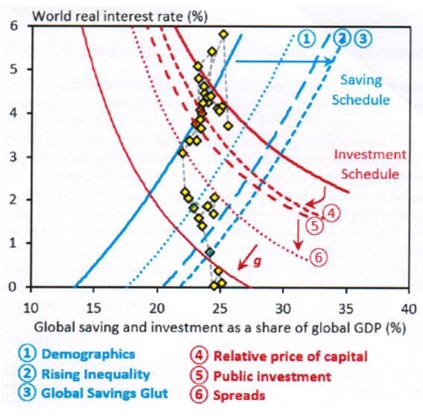

The US economy - by size and depth the nearest to a closed economy model – has witnessed a steady decrease of real interest rates over the past decades, from 4-5 percent toward almost zero at present (Williams and Laubach, 2003; King and Low, 2014;Summers, 2014; Haldane, 2015; Williams 2016, etc.). In the global economy, which may be viewed as a closed one, real equilibrium interest rates had also fallen steadily over the past three decades (Figures 1&2; Rachel and Smith, 2015; Holston, Laubach and Williams, 2016); figure 2 mentions factors that moved global saving and global investment.

Lawrence Summers argues that the equilibrium rate, which allows full capacity utilization, is negative at present ( 2014, 2016). But a legitimate question is posed by the pretty low unemployment rate in the US, which is below 5 percent currently; is it a sign of massive under-utilization of resources? Such a figure should nevertheless be adjusted for labor market participation and income levels.

If the severe unemployment case is dismissed, how does it come that inflation does not pick up? And why are inflation expectations persistently so low? It may be that, as James Bullard argues, there is need for another narrative . The latter should be centered on a Fisher equation ( i = ir + π exp), where (i) is the nominal interest rate, (ir) is the real rate, and ( π exp) is expected inflation; the line of reasoning is that, under conditions of persistent low inflation, and when output and unemployment gaps almost disappear, the Taylor’s rule turns into a Fisher equation [5]. Bullard suggests that since the real rate is determined by markets, the “pegging’’ of policy rates can be put in relation with persistently low inflation expectations. It may be that markets take their cues from resilient low policy rates. And there can also be a ‘’regime shift’’, which depends on productivity growth, real interest rates on short term government bonds, and the state of the business cycle. Optimal monetary policy is regime dependent. But, would this policy rate pegging and its impact on inflation expectations imply that policy rates need to climb again in order to move inflation expectations upwards? This would fit into BIS’view that policy rates need to move upwards to combat new speculative bubbles. On the other hand, what if markets would not see it as a credible policy change, and inflation expectations may continue to stay low due to low economic growth, low productivity, demographics? And what if raising the policy rate would be, yet, premature by risking a new recession? In any case, this is a huge policy conundrum[6].

Two key issues emerge: a/ whether negative equilibrium interest rates are justified, and b/ whether negative policy rates are effective? If resource allocation were adequate, the equilibrium rate should not be below zero. It is economic common sense to think so. But there is a different story when resources are grossly misallocated and structural conditions are unfavorable. During massive and chronic under-use of resources intense hysteresis may take place. Such circumstances may erode not only the value of current resources, but potential GDP too. Therefore, there are arguments for policy intervention to exit the state of considerable under-use of resources and to avoid deflation, debt-deflation. If such arguments (the ECB’s current stance now, for example) are accepted, the issue that needs to be clarified is what kind of a policy mix should be used in the context of non-standard measures (such as those adopted by various central banks and which have entailed side effects (among which speculative bubbles and the impact on non-banks’ financial balance-sheets).

Another important question is linked with resource misallocation and heightened bad distributional effects (Stiglitz, 2016) when policy rates are very low. Summers, in his secular stagnation argument, says that there is a trade-off between the need to boost output and financial stability, while monetary base expansion is fueling the search for yields and new speculative bubbles (2014). Therefore, he calls for increased resort to fiscal tools. According to Bradford DeLong and Lawrence Summers (2012), the main reason would be that at very low interest rates high budget deficits should not be a cause for concern, and that extra deficits would be easily financed via an increased fiscal multiplier and a rise in potential GDP. This state of affairs would be the case in a depressed economy. As they say “...although the conventional wisdom articulated by John Taylor (2000) rejecting discretionary fiscal policy is appropriate in normal times, such policy has a major role to play in a severe downturn in the aftermatch of a financial crisis that carries the interest rates down to the zero nominal lower bound (2012, pp.233). DeLong and Summer’s view appears to gain traction when monetary tools lose much of their effectivesses and helicopter money would rather be avoided as an alternative policy tool. Nota bene: what seems affordable for the US economy (which issues the main reserve currency of the world) is not necessarily affordable in emerging economies facing inherent vulnerabilities (ex: high currency substitution dollarization/euroization).

Figure1: the fall of real rates in the world (1980-2015)

Source: Rachel and Smith, who quote King and Low (2014), Consensus Economics, IMF, Datastream

Figure. 2: shifts in saving and investment schedules in the world ecnomy (1989-2015)

Source: Rachel si Smith, 2015

Negative policy rates?

When inflation is persistently very low, policy rates can hit the zero lower bound. If real rates need to be negative to bring output to its potential and avoid damagin hysteresis ( high structural unemployment, erosion of potential GDP) a dilemma and a technical problem appear: is it possible to take policy rates into negative territory? Looking at the past years’ experience, the technical barrier can be overcome up to o point. However, the policy dilemma remains.

Massive capital movements complicate the picture. This is what Mario Draghi pointed out at the ADB’s annual meeting in Frankfurt by referring to the balance between investment demand and the supply of saving[7]. Such a statement is well substantiated if one takes into account not only the savings glut (Bernanke 2005) in the global economy following past decades’ development in China (where savings account for almost half of household income) and Asians and East Europeans’ low wages in a global competition which favored disinflation and deflation pressures. Moreover, the euro-area, which is highly divided in terms of competitiveness (North and South division) is showing a current account surplus of cca. 3 percent of GDP (2015), which is also putting pressure on the global investment and saving balance.

An economy may have an initial internal investment-saving equilibrium, but if massive capital inflows take place, interest rates may fall dramatically; output may exceed its potential for a while and speculative bubbles will quite likely occur. A speculative bubble emerged in the euro-area periphery, in the EU’s emerging economies, where external imbalances grew dramatically in the precrisis years. It has also happened in the global economy due to recent QEs, which moved much liquidity to emerging economies.

The financial crisis led to a dramatic drop in investment and boosted saving. According to various estimates, average investment fell to 17-18 percent of GDP in the EU from 22 percent before the crisis. A basic question is whether the ECB has enough reasons to set negative policy rates; the debate cannot ignore the currency war in the global economy (a depreciated euro versus the US dollar can help the euro-area periphery), debt-deflation fears[8], as well as how to discourage savings in a bid to boost consumption, etc.

All in all, real interest rates are low as a result of developments in the investment-saving balance. Central banks’ moves may try to influence short-term rates, but, over the longer run, these steps are effective only if economies get out of the doldrums and the erosion of potential GDP is limited. Central banks cannot be all-problem solvers; reform measures are needed to address structural weaknesses which relate to demography, education, public investment, innovation, etc;fiscal policy may have to play a stronger role.

Can equilibrium rates be pushed upwards?

Should central banks raise policy rates , for instance for reasons linked with an assumed policy shift? In Europa, this issue is rather complicated as the increase in credit cost along with a higher saving propensity (amid rising interest rates) might push the European economy back into recession, into a possibly new acute crisis with deteriorating again bank balance sheets). A factual example is Sweden a few years ago, where Riksbank tried to stem the boom in the mortgage market by raising the policy rate; that pushed the economy back into recession, as Lars Svensson (who was deputy governor at the time) feared[9]. The fear of new recession is legitimate[10].

Moreover, could large central banks induce an upward thrust in real rates in the global economy above the level implied by structural conditions? In the short run, maybe yes. Assuming concerted actions, such a development can be imagined. This actions would imply a massive absorption of liquidity (of base money), a large-scale drainage via sizeable bond sales that will take yields higher, would strain financial markets again, induce a new recession episode, heighten the debt-deflation threat, and trigger a string of bankruptcies. Banks will face major asset losses similar to those in central banks’ balance sheets (though, some may say that these losses should not be a concern for the issuer of a currency even in case of political impediments). Markets would freeze anew by forcing central banks to, supposedly, intervene again in the reverse. Therefore, structural changes are needed for long-term equilibrium interest rate to pick up; this means productivity growth, demographics, uncertainty, etc.

Returns on savings are slim, or almost nil, and insurers and private pension funds are hurt. But it is unfair to blame recent years’ policies for the structural conditions in the global economy. The cheap money policies of the Great Moderation period, when massive misallocation of resources and the global financial cycle were fueled, is an issue for debate however.

Emerging economies

Small and large emerging economies are trapped in this highly complicated and uncertain environment and bear the fallout from speculative capital flows. Countries with large budget and external deficits, high external debt, are more vulnerable and prone to balance of payment crises. The fall in commodity prices is also hitting hard countries which rely on basic commodity exports.

European emerging economies have undergone remarkable macroeconomic adjustments in recent years. They have an apparent advantage since their overall public and private debt is almost half as a share of GDP compared to developed EU countries (their legacy problem is much smaller). Likewise, their USD exposure is relatively low, which protects them somehow from the impact of Fed policy changes. But they are facing significant dilemmas:

- if inflationary pressures grow, should central banks in these countries raise policy rates while the ECB and other central banks continue setting very low, even negative rates? Would such moves lure speculative capital inflows? It is worth mentioning that wherever there is a gap between money markets and policy rates, it may dampen speculative inflows[11].

- is it reasonable to foster a reduction of the currency substitution (euroization) by all means when euro adoption is mandatory at one point[12]? One may be tempted to say yes due to the rise in the room for maneuver of monetary policy

- If the Impossible Trinity (autonomous monetary policy, stable exchange rate, and free capital movements) is actually a dilemma (as Helene Rey says), then capital controls are needed – be they under the guise of macro-prudential measures. IMF itself has reassessed the appropriateness of capital controls. These measures require a good coordination among central banks, regulators [13];

- The ECB should ensure facilities similar to those available in the euro area, given the integrated EU financial market, the heavy presence of foreign banks from the euro area in the non-euro-area banking sectors, the high currency substitution (euroization) in some of these economies.

High liquidity and, yet, major sudden stop threats

Fresh financial market turmoil cannot be automatically prevented via lower real interest rates and an expansion of high-powered money in the global economy; markets may freeze again and balance of payment crises may occur if large macroeconomic imbalances operate. Unconventional shocks can also frighten markets. Real rates were actually low even in the pre-crisis years. The global financial system is rife with vulnerabilities, not least because of a higher degree of interconnectedness, high leverage, and sophisticated financial instruments. In spite of more severe capital and liquidity requirements, of a new regulatory and supervision regime, transmission mechanisms continue to be precarious and sudden stops may emerge in areas of capital (money) markets, triggering contagion. This poses a tremendous challenge for governments and central banks, the latter having exhausted much of their ammunition. This is why some voices (Adair Turner, Willem Buiter) mention helicopter money as a solution to repair financial intermediation. But this distribution of free purchasing power is not devoid of threats. On the other hand, if there is enough fiscal space, a boost in public spending may be used especially when it would target clear domains (like infrastructure), which can have a strong impact on the whole economy and would bolster aggregate demand.

The still fragile financial system is mirrored by developments across shadow banking, by systemic risks which evolve in capital markets. One should not rule out that the lender-of-last-resort function would be called upon for such markets too. The bottom line is that there is need for continuing reforms of finance in view of the risks posed by interconnectedness, the too-big-to-fail syndrome, bad practices of this industry. A simpler and more transparent financial system, a reform of the international system aimed at cushioning negative externalities are badly needed.

Final remarks

Let’s sum up with a few inferences

- structural trends, oversize finance, and a drifted financial cycle provided the conditions for the eruption of the financial crisis;

- the slowdown of the global economy (which is due to structural factors) was obvious before the eruption of the financial crisis;

- structural factors have changed the propensity for investment and saving . Against this background, real interest rates have turned much lower since long;

- over-indebtedness is a huge burden; it may be softer in the US where capital markets are well developed, whereas the EU relies heavily on banks, with their overloaded balance-sheets. The reduction of huge debts (deleveraging) is a lengthy process;

- when inflation is so low, central banks may need negative policy rates to produce negative real rates –this is a big novelty in today’s world ( Carmen Reinhart[14]).

- income inequalities create tensions in society; this is fueling populist and protectionist movements in both developed and emerging economies; globalization limits come to the fore;

- can new technologies bring in a new upswing? Can a better resource allocation, able to alter the distortions caused by policy errors and the exuberance of the past decades, help? It is not impossible, but it is time consuming given that debts are high, the financial sector is still fragile, and there are numerous tail events, big uncertainties;

- global economic conditions are extremely unusual (the New Normal), fueling great confusion and uncertainties;

- limits of cognitive models are increasingly clear and policies are navigating unchartered waters; but we can take comfort in the fact that a generalized Great Depression was avoided, at least until now;

We need patience. We need to bank on the reinvigorating force of the entrepreneurial spirit and pragmatic policies (some call them non-standard). There may be a recovery underway, be it a very slow one. It is too early to speak about the long term future of economic policies. And there are fundamental aspects still to be clarified better. Are substantial negative equilibrium rates to be seen as normal? Are negative policy rates effective? If resource allocation were adequate, natural rates should not go below the zero-lower bound. Should we target a higher inflation rate ( as Olivier Blanchard, John Williams, and other economists recommend) to reinforce the monetary policy instrument? This looks to be wishful thinking in the current circumstances, even though in theory it seems to make sense.

References

- Bernanke, Ben, (2005), “The Global Savings Glut and the US Current Account Deficit” Sandridge lecture, Virginia Association of Economics, Richmond, Virginia

- Blanchard Olivier, (2013) “Monetary policy will never be the same”, VoxEu, 27 November

- Borio, Claudio, (2012) “The financial cycle and macroeconomics: what have we learned and what are the policy implications”, BIS Working papers no.395, December, and in Nowotny et.al (2014)

- Borio, Claudio, (2014) “The financial cycle, the debt trap and secular stagnation”, presentation the BIS General Meeting, Basel, 29 June

- Borio Claudio and Piti Disyatat, “Low interest rates and secular stagnation: is debt a missing link?”, Voxeu, 25 June 2014

- Borio, Claudio, Enisse Karroubi, Christian Upper, Fabrizio Zampoli (2016), “Financial cycles, labor misallocation, and economic stagnation”, Voxeu, 14 April, 2016

- Bullard, James, “A tale of two narratives”, presentation, Saint Louis Fed, July 2016

- Caruana, Jaime, (2014), “Stepping out of the shadow of the crisis: three transitions for the world economy”, speech at the General Meeting , BIS, Basel, 29 June

- Calvo, Guillermo, “From chronic inflation to chronic deflation”, paper presented at the World Bank conference “The state of economics”, 8-9 June, Washington DC, 2016

- Constancio, Vitor, “The Challenge of low real inrerest rates for monetary policy”, lecture, The Macroeconomics Symposium, Utrecht School of Economics, 15 June, 2016

- Den Haan, Wouter (editor) (2016), “Quantitave Easing:, CEPR Press, E-Book

- DeLong, Bradford and Lawrence Summers, 2012, “Fiscal policy in a Depressed Economy”, Brookings Papers on Economic Activity, Spring

- Draghi, Mario, 2016, “Addressing the causes of low interest rates”, Introductory speech at the Annual Meeting of the Asian Development Bank, 2 May

- Eggertson, Gauti, Neil Mehrotra, and Lawrence Summers, “Secular Stgnation in the Open Economy”, The American Economic Review, Papers and Porceedings, May, 2016, pp.503-508

- Evans, George W. and Bruce McGough, “Interest rate pegs in New Keynesian Models”, April 26, 2016

- Holston, Kathrin, Thomas Laubach and John Williams, “Measuring Natural Rates of Interest. Trends and Determinants”, FRBSF, Working Paper, June 2016

- Gordon, Robert J (2014), “The demise of US economic growth: restatement, rebuttal and reflections”, NBER Working Paper, No. 19895

- - Koo, Richard, (2011), “The World in balance-sheet effect recession: causes, cure and policies”, Real World Economics Review, Issue No.58

- Korinek, Anton and Jonathan Kreamer (2014), “The Redistributive effects of financial deregulation: Wall Street vs. Main Street”, BIS Working Papers, No.468, October

- King, Mervyn and David Low (2014), “Measuring the “world real interest rate””, NBER, Worging Paper

No.19887

- Jobst, Andreas and Huidan Lin, “Negative Interest Rate Policy (NIRP): Implications for Monetary Transmission and Bank Profitability in the Euroaria”, IMF Working Paper, WP/16/172, 2016

- Laubach, Thomas and John Willams, 2003, “Measuring the Natural Rate of Interest”, The Review of Economics and Statistics, 85(4), November

- Minsky, Hyman, “John Maynard Keynes”, New York, McGraw Hill,1976 (reprinted 2008)

- Minsky, Hyman, “Stabilizing an unstable economy.” (first published 1986), New York, McGraw-Hill, 2008

- Ostry, Jonathan D., Andrew Berg and Charalambos Tsangarides (2014), “Redistribution, Inequality and Growth” , IMF Discussion Note, February

- Reinhart, Carmen (2016), “What is new about todays’s low interest rates?”, Project Syndicate, 28 July

- Rey Helene, “Dilemma not Trilemma: The global finaqncial cycle and monetary policy independence”, Global Dimensions of Unconventional Monetary Policy, proceedings of the Federal Reserve Bank of Kansas City Symposium, Jackson Hole, 22-24 August, 2013

- Rachel, Lukasz and Smith, Thomas, 2015, “Secular drivers of the global interest rate”, Bank of England, Staff Working Paper No. 571

- Stiglitz, Joseph (2016), “What is wrong with negative interest rates?”, Project Syndicate, 13 April

- - Stiglitz, Joseph, (2010), “Contagion, Liberalization, and the Optimal Structure of Globalization”, The Journal of Globalization and Development, Volume 1, Issue 2

- Summers, Lawrence, 2014, “Reflections on the New secular Stagnation Hypothesis”, in C.Teulings and R. Baldwin (eds), “Secular stagnation: facts, causes and cures”, VoxEU.org eBook, CERP Press

- Summers, Lawrence (2016), “The Age of Secular Stagnation”, Foreign Affairs, March/April

- Teulings Coen and Richard Baldwin, (2014) “Secular Stagnation: facts, causes and cures”, a VoxeBook,

- Turner, Adair, “Demistifying Monetary Finance”, Voxeu, 10 August 2016

- Vinals, Jose, Simon Gray, and Kelly Eckhold, “The Broader View: The Positive Effects of Nominal Negative Interest Rates”, IMF blog, 10 April 2016

- Williams, John, “Monetary Policy in a low R-star World”, FRBSF Economic Letter, 15 August, 2016

* text based on a presentation made at a BIS seminar on Monetary Policy issues in Emerging Economies, Skoplje, March, 2016. A larger version has appeared as NBR Occasional Paper, No. 15, 2016. Comments made by Mihai Copaciu, Laurian Lungu, and Radu Vranceanu are acknowledged. The author bears sole responsibility for the views expressed herein.

[1] Mario Draghi, speech at the ADB annual meeting in Frankfurt, the ECB website ( 2016). Vitor Constancio ( 2016)

[2] Jose Vinals, Simon Gray, and Kelly Eckhold (2016). But an IMF staff paper argues that, at some point substantial interest rate cuts may outweigh the benefits from higher asset values and stronger aggregate demand. And that monetary accommodation may need to rely more on credit easing and an expansion of the ECB’s balance sheet (Jobst and Lin, 2016)

[3] Hyman Minsky, “’John Maynard Keynes”’ (1975). This thesis is further elaborated in his “Stabilizing an Unstable Economy”’

[4] In practice, a central bank cannot take policy rates much below zero. There is a limit to how far central banks can lower their rates into negative territory. If commercial banks pass on the costs to their clients we could witness a variant of a bank run as clients rush to withdraw their savings. Though, such an inclination may be offset by the need to manage personal cash holdings, by transaction and protection costs.

[5] In the circumstances of zero interest rate policy (ZIRP), of “permazero”’, which has, arguably, characterized G-7 in recent years, a Taylor rule collapses into a Fisher equation. Thus, i = ir + π (exp) + µ π(gap) + β Q (gap) = ir + π (exp), where (i) is the nominal policy rate, (π (exp)) is expected inflation, (ir) is the real interest rate, and output and inflation gaps are considered. When the unemployment and the inflation gaps close (which is mostly the case of the US economy currently) the Taylor rule turns into i=ir+ π (exp), a Fisher equation (James Bullard, “A tale of two narratives”, presentation, Saint Louis Fed, July 2016). See also his “Permazero in Europe”, International Research Forum on Monetary Policy, Frankfurt am Main, 18 March, 2016 (attention at equations!!!)

[6] See also Evans and McGough(2016)

[7] See also Gauti Eggertson, Neil Mehrotra, and Lawrence Summers (2016)

[8] See also Guillermo Calvo (2016)

[9] “Central Banks: Stockholm Syndrome”, Financial Times, 19 November, 2014

[10] Ther are here two additional questions. What if the ECB intervention was distortionary in the first place and now the answer should rather be a policy reversal; second, what if the first ECB intervention (after 2008) was right, in order to address liquidity issues, while solvency related ECB intervention was less appropriate. Both questions need an answer to the issue of banks’ legacy and the burden distribution across the euroaria. The problem with both these two questions, however, is that the ECB was the only institution that could intervene in order to rescue the Eurozone. Moreover, distinguishing between liquidity and solvency problems is quite complicated in the real world.

[11] It is the so-called Tošovský dilemma, specific to inflation targeters.

[12] Though it is fair to say that euro adoption makes sense when the euroria would have overhaluled its policy design and arrangements and a candidate economy would have achieved a proper degree of real and strictiral convergence.

[13] The 2006-2008 experience indicates that the strong rise in real credit growth was also stimulated loan externalization practiced by foreign banks’ subsidiaries.

[14] “’…during and after financial crises and wars, central banks increasingly resort to a form of taxation that helps liquiditate huge public and private debt overhang…financial repression…today this means consistent negative real interest rates…more poften than not, negative real interest rates were accompanied by higher inflation (as during wars and in the 1970s), than we observe today in advanced economies…”(Carmen Reinhart, 29 July, 2016)