- Regain price stability without endangering other macroeconomic equilibria.

- Tailor the pace of disinflation as to avoid conflicts with financial stability.

- Sail through short term trade offs to achieve long term objectives - usually the long standing case for EME.

After almost two years of battling price pressures by embarking on one of the most aggressive hiking cycle in economic history, central banks seem fully committed to go even further with their tightening campaign to rein in runaway inflation should the case be.

This is a battle that central banks can’t afford to lose. Price stability is the ethos of monetary policy and central banks shall remain resolute in their purpose to return inflation to target and preserve their hard earned credibility. But the devil is in the details and even though the destination is well know, there are many unchartered paths and possible journeys, whose choice will reverberates in the years to come.

I believe that central banks might be at a crossroad right now. The tightening cycle risks going into overdrive and the price stability objective could collide with financial stability. In their quest to return inflation to their aim, central banks risk becoming inflation nutters and disregard financial stability considerations. In central banking jargon, the fear of overkilling looms large right now.

The hard conclusion of this paper is that there may be instances where financial stability considerations should inform monetary policy decision, even though financial stability is not a de jure monetary policy goal.

This column is not framed as an academic paper that thoroughly analyzes different dogmas or school of thoughts regarding the evolving nature of the interlinkages between price stability and financial stability. Rather, the paper will be tailored as a policy paper that delves into the conduct of monetary policy during the ongoing tightening cycle, tries to assess the recent progress and to convey some policy recommendations going forward.

What is the hallmark of the ongoing tightening cycle and how higher rates percolated through the economy? Why economic activity is so resilient and price pressures so persistent despite this aggressive tightening cycle? What are the boundaries between price stability and financial stability and where is the breaking point that tilts the balance between costs and benefits of monetary policy actions?

1. What is the hallmark of the ongoing tightening cycle and how higher rates percolated through the economy?

Compelled to tighten and remove accommodation. Central banks relied, for a period, on the mantra of transitivity. The shift in the inflation narrative around the world and the vanishing of the transitory theme prompted forceful actions by major central banks and ignited a race to normalizing monetary policy stances. Rate markets received large vibrations and quickly repriced higher for an aggressive hiking cycle.

As more and more central banks changed course, policy rate expectations and financial markets developments quickly went into overdrive. Uncertainty regarding the future course of monetary policy rapidly took hold as no one knew (not even central banks themselves) how fast, how far and for how long rates should need to go. Both policy makers and market participants were sailing in deeply uncharted waters.

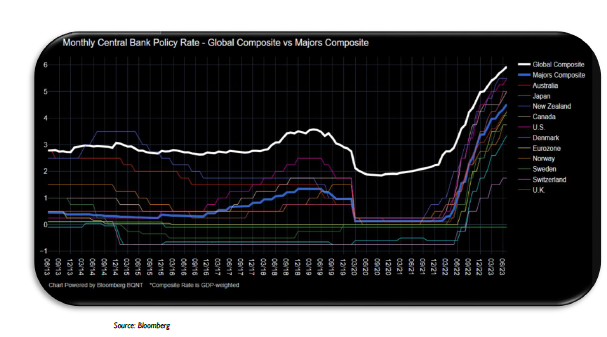

Competitive tightening shortly emerged. Although the timing, speed and magnitude of policy normalization varied at first, the pace and intensity of policy actions of central banks rapidly converged as the world faced a common challenge: a staggering unexpected rise in inflation and the imperative of central banks to preserve their anti-inflationary credentials.

Central banks undeterred to hike by global market rout. Abrupt reappraisals of policy rate expectations sent ripple effects across all corners of financial markets. Despite global market routs and downbeat market sentiment, central banks worldwide seemed undeterred to hike and relentlessly pursued their tightening campaign.

This was one of the most sudden monetary policy turnarounds in living memory. The financial world was forced to cope with a rise in global tides of monetary policy tightening at a speed and magnitude that were inconceivable not long before.

In a summit push at higher altitude the pace naturally slows. As policy rates approached natural rate of interest in most part of the world, central banks turned more cautious in further altering their policy rates and downsized their tightening pace to lower clips of 50 bp and 25 bp and then endorsed a new approach coined higher for longer.

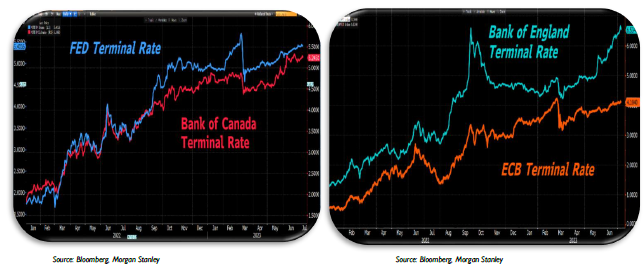

Terminal rate constantly pushed higher. As central banks embraced an outright hawkish approach and became less minded to wait, the end point of the hiking cycle moved in lock steeps. The below two charts describe the evolution of the terminal rates for the four most important central banks. These rates are inferred from market prices by Morgan Stanley and are provided by Bloomberg. As it can be seen, the speed as well as the magnitude of reappraisals of the peak rate in the current tightening cycle were unparalleled in recent history.

High uncertainty regarding the reaction function led to monotonically increasing forward rates. The large magnitude of interest rate adjustments, as well as the unexpected gyration in terms of central bank communication were a notable departure from previous policy practices in terms of clarity and gradualism. As a result of rapidly changing economic conditions, central banks abandoned the forward looking approach and endorsed a data dependent approach in which they started to take decisions meeting by meeting.

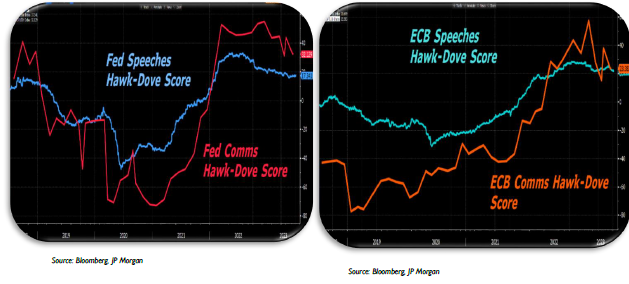

Hawkish communications and completely non committal approach. Monetary policy is not only about setting interest rates but also about managing expectations. Security markets and long term investment decisions are inherently forward looking and reflect a constellation of current and prospective changes in the state of the economy. Beliefs about the future are meant to shape current behaviors. As a result policy statements and speeches came under intense scrutiny by market participants in order to infer possible signals about a perceived change in monetary policy. Using Natural Language Processing (NLP) JP Morgan developed a large language model used to gauge the hawkishness or dovishness of communications and speeches, called JP Morgan Hawk-Dove Score.

Swift and complete pass through from origin to all corners of the financial market. The transmission of monetary policy to financing conditions has proven relatively swift and complete.

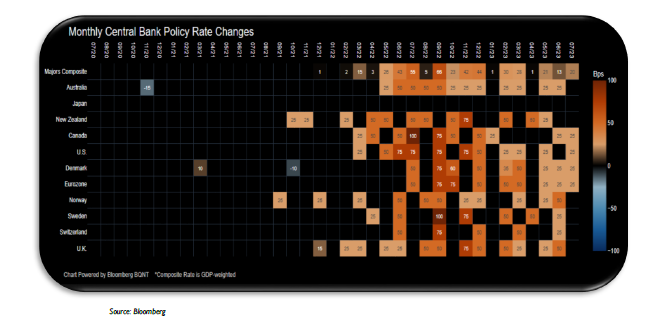

ECB deployed 9 hikes which amounted to 425 basis points of cumulative tightening over one year window. FED was even bolder and increased the policy rate 11 times for a 525 basis points of cumulative tightening over a time span of 15 months.

In order to assess the strength of the monetary policy transmission mechanism and evaluate the journey of monetary policy impulses from origin to destination, I will deploy indicators that are usually used in central bank practice to assess the monetary policy stance. Because the relative importance of each indicator could be time dependent and state dependent, I decided to use alternative metrics in order to avoid over reliance on one variable or forecast.

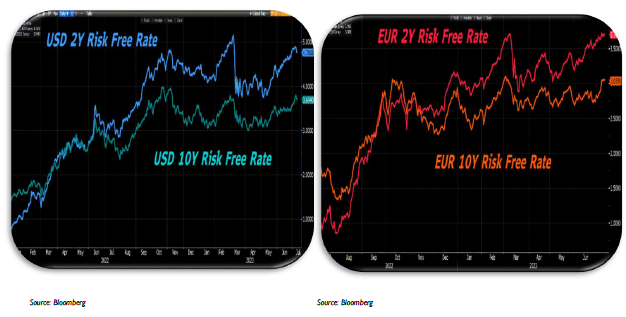

Tightening upstream financial conditions as policy rate expectations went ballistic percolated to downstream financial conditions. Risk free rates (RFR) have climbed dramatically as the hawkish pivot has let market participants to discount faster and bigger rate hikes as well as higher terminal rates. Moreover, as more hikes have been priced in the end point for the hiking cycle was constantly pushed forward.

RFR with a 2 year maturity denominated in EUR and USD - usually sensitive to prospective changes in policy rate – increase from - 0.40 percent (January 2022) up to 3.70 percent (July 2023) in the former and from 0.75 percent (January 2022) up to 4.80 percent in the latter. In the same vein, RFR with 10 year maturity increase from 0.14 percent up to 3.05 percent in Eurozone and from 1.45 percent up to 3.70 percent in US.

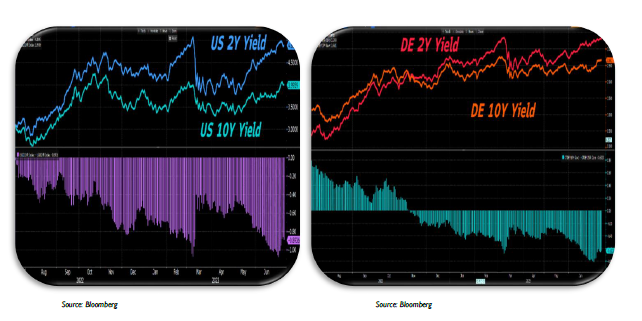

Swift pass through from RFR to bond markets and…The repricing of monetary policy rate expectations has been transmitted to broader fixed income markets beyond RFR. As a result, government bond yields have risen in lock step with RFR given the contributions from both components: rate expectations and term premium. Moreover, the term structure constantly flattened / inverted as the repricing of monetary policy path weighted heavily on short and interim maturities and then monotonically dissipated through the curve.

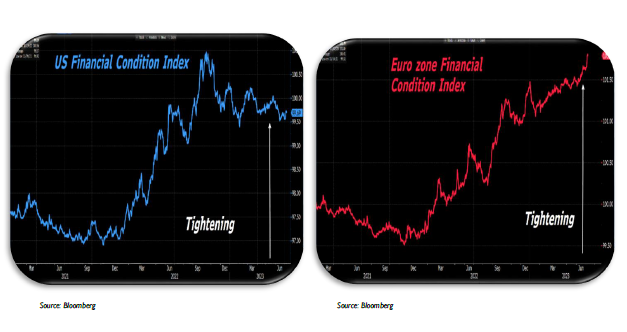

….further out to broader financial conditions. Reassessment of monetary policy stance and recalibration of monetary policy instruments translated to broad financial conditions. The below financial condition indexes calculated by Goldman Sachs provide a comprehensive assessment of overall financial conditions for a wide range of business and households in the euro zone and US. Those indexes embody a large variety of interest rates and prices for different segments of financial markets. As it can be shown, removing policy accommodation reverberated to both upstream and downstream financial conditions, pushing higher the overall cost of credit for the real economy.

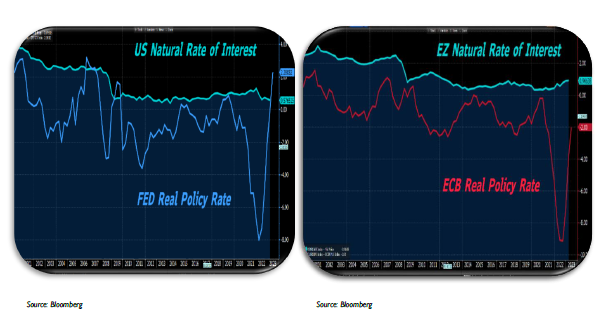

Policy gap closed fast. Another indicator used to assess the orientation of monetary policy is the deviation of real policy rate from the natural rate of interest. The natural rate of interest is not an observable variable and could only be inferred by using complex econometric modeling. Moreover, the natural rate of interest is constantly changing, even shifting. I use one of the most closely followed approximation of natural rate of interest provided by Federal Reserve Bank of New York and estimated by Laubach Williams and Holston Laubach Williams Models[1].

We can see below that, in the case of the European Central Bank, the actual policy rate is still lagging behind and there is more tightening ahead just to reach natural rate - a policy stance that is neither accommodative nor restrictive. Nevertheless, rates climbed fast from very low /negative levels and a significant tightening come also from balance sheet run offs.

The Federal Reserve System has already entered into restrictive territory as it is running a positive policy gap

Taylor Rule points that rates are peaking.The last complementary measure that I use to assess monetary policy orientation is to compare the monetary policy rate with predictions inferred from monetary policy rules. The most common one is the Taylor rule, which is currently a key component of most modern macroeconomic models, many of them used by central banks for policy analysis.

Model based estimates provide a useful assessment of the strength of monetary policy stance. Nevertheless, periods with heightened uncertainty or marked by forceful policy action required caution in using model based on regularities.

MPR = ρ MPR (t-1) + (1-ρ) [ r* + α (π t – πt*) – β ( ut - ut *) ]

Where MPR is the monetary policy rate, r* is nominal r-star, π is inflation, π* is the 2% inflation target, u is the unemployment rate, and u* is the natural unemployment rate. The parameters α (alpha) and β (beta) calibrate how much the Fed reacts to changes in core inflation and unemployment. ρ is the smoothing parameter that reflects the fact that policy rate generally adjusts slowly to macroeconomic data. A value of 1 for α is in the lower bound of possible values that could be assumed in macroeconomic models with stable inflation dynamics

The parameter of unemployment, β, is calibrated using the original output parameter from the Taylor rule suggested by Taylor (1993) (equal to 1/2), multiplied by 2, the value of Okun's law parameter linking output to unemployment. Finally, the smoothing parameter ρ is set to 0.8, and comes from Smets and Wouters (2007)[2].

I run estimates for ECB and FED monetary policy rates based of aforementioned specification using Bloomberg. The Taylor Rule estimation provides a monetary policy rate of roughly 6.60 percent for FED (5.25 percent currently) and 5.50 percent for the ECB (3.5 percent currently).

Judging after the current and expected level of policy rates inferred from market prices in both cases it could be the case that there is slightly more ground to cover. Therefore, there is a slight contrast with current market prices which are discounting 2 more hikes for a cumulative of 50 bp in both ECB and FED cases.

Nevertheless, the estimates should be treated with caution because these are not hard numbers/guidance to how far monetary policy should go but rather a framework used to reinforce/support the judgment used in policy analysis.

Moreover, during this cycle, the tightening of monetary policy stance encompasses large balance sheet shrinkage and liquidity absorption which are not captured by Taylor rules.

[2]Smets,FrankandRafaelWouters.2007.“ShocksandFrictionsinUSBusinessCycles:A BayesianDSGEApproach.”TheAmericanEconomicReview,586–606

Strong transmission so far. Front loading the hiking cycle and shrinking balance sheets by all developed central banks were increasingly feeding through the entire constellation of interest rates and prices, rendering monetary policy stance significantly restrictive.

In line with economic theory and past tightening cycles, the first segment of the monetary policy transmission mechanism (policy rate – financial system) was pretty efficient. Monetary policy impulses have been channeled swiftly and almost completely.

2. Why economic activity is so resilient and price pressures so persistent despite this aggressive tightening cycle?

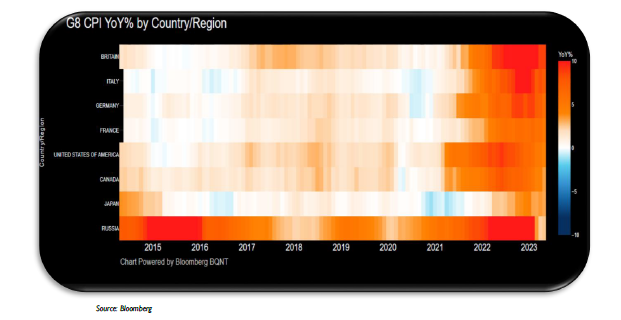

Hard to disentangle signals from noises. Global economy was hit by overlapping negative supply shocks which pushed inflation far above central banks’ tolerance bands. A material shift in consumption patterns from services to goods, in conjunction with constrained production capacities were the precursor of rising inflation as supply and demand mismatches emerged. The war in Ukraine prolonged price pressure from prior supply bottlenecks with an additional layer of supply shocks to food, energy and other commodities. Inflation rates in G8 countries rapidly increased towards double digits and stabilized at levels not seen in decades.

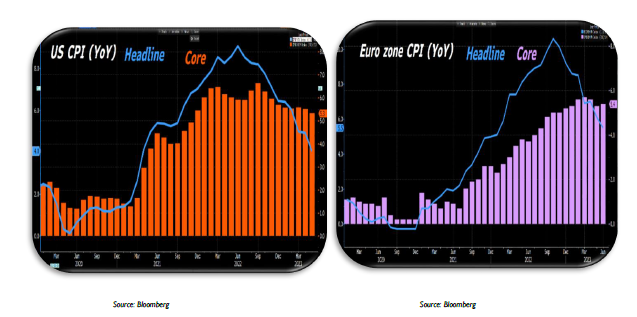

Perfect symmetry of factors driving the rise and fall of headline inflation. In the US, headline inflation rate peaked at 9.1 percent in the second half of 2022 and reversed to 4 percent only towards the beginning of 2023, as adverse supply side shocks started to dissipate and base effects kicked in. The same factors that pushed prices higher after the outbreak of the pandemic and the war in Ukraine acted in the opposite direction, restraining price pressures. Despite these favorable developments, core inflation proved stickier that previously envisaged and still hovers marginally above 5 percent, after peaking at 6.6 percent.

In Eurozone the picture is broadly the same. While headline inflation rate crested at 10.6 percent towards the end of 2022 just to eased down to 5.5 percent in the following year, core inflation remains near close to peaks at 5.40 percent.

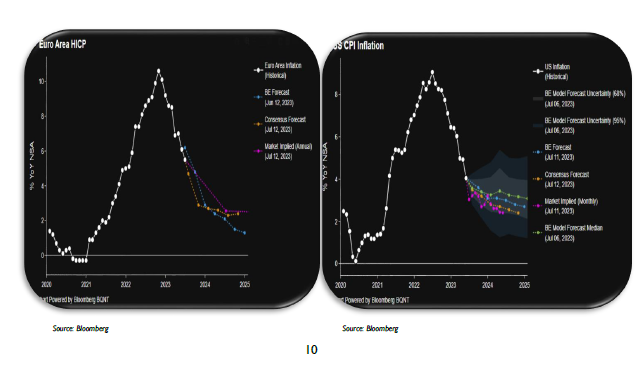

It seems the tide of inflation has turned but... The reversal of these shocks towards the end of 2022 and beginning of 2023 dampened price pressure and supported the rolling over of inflation in all jurisdictions.

A forward looking analysis is showing that inflation is projected to slow further as energy and food inflation continues to cool down and supply bottlenecks ease definitely. Moreover, restrictive monetary policy will continue to dampen demand.

…still too high to be complacent. Nevertheless, despite both current and anticipated decline, inflation is considered to remain uncomfortably high. This level risks destabilizing inflation expectations and generating second round effects and price – wage spirals. Moreover, inflation excluding energy and food is proving stubborn and more persistent than initially thought. This time around, price pressures seems broader based and the disinflation process is taking a longer time to materialize.

Change in inflation anatomy. In order to understand the prospects of inflation and its changing nature, I shall try to disentangle the factors that underpinned the strength and persistency of inflation. In this regard I shall emphasize two broad categories, one related to 1) price and wage setting behavior and the other related to 2) monetary policy transmission mechanism. Of course, the relative importance of this factors varies from one jurisdiction to another, given different economic structures and policy responses.

1) Price and wage setting behavior

Perfect conditions that facilitated the transmission of pipeline price pressures. Inflationary pressures reverberate through the economy in stages as economic agents pass the changing costs to each other at different moments in time. Broadly speaking, the companies’ mark up is conditional on the wider economic cycle and the strength of demand for the respective products/servicea, as well as the degree of competition within the respective industry.

At the beginning, the supply side shocks led firms to swiftly react to higher input costs and pass the burden on to consumers in order to defend their margins. This is the usual response of economic agents to an averse terms of trade shocks. Nevertheless, the ability to transpose the pipeline price pressures further up the chain rests on the state of economic activity, which this time around favored the preservation of profit margins.

As economies reopened, forced savings, pent up demand and expansionary policies gave companies more scope to pass on higher costs to consumers. Tight labor market and structural shortages in some sectors will continue to increase wages and therefore unit labor cost, given tepid productivity growth. Moreover, in an attempt to regain purchasing power, workers will continue to push for higher wages.

As time passes, the squeeze of income from higher prices and the restrictive monetary policy stances will weigh-in on economic activity. Tightening financial condition will reverberates at first to sectors that are more sensitive to interest rate cycles. That is what is happening to manufacturing and construction. Higher for longer policy rates will squeeze demand and force companies to absorb rising input costs, including wages.

2) Monetary policy transmission mechanism

Some factors reshaped the transmission of monetary policy impulses. The current economic context most probably slowed the speed and magnitude of the transmission of monetary policy impulses form financial markets to aggregate demand and inflation – slower efficiency of the second and third segments of monetary policy transmission mechanism. There are a few reasons worth emphasizing that could have worked in this direction.

First, the proportion of fixed term loans has increased in the last decade, especially in euro area countries and UK. This tendency is prone to slow the pass through of monetary policy rates to the outstanding stock of loans and delay the tightening of the cost of credit to the real economy. Also, a higher share of fix term loans basically shielded households’ cash flows from higher rates, enhancing borrower balance sheet channel. Moreover, nominal rigidities of prices and wages, which are a hallmark of euro area and other European countries, also further dampened the transmission.

Second, the current tightening cycle started from deeply negative real interest rate levels and just only recently monetary policy stances of major central banks started to turn restrictive or sufficiently restrictive. If we look at the FED, the policy gap already closed and the real policy rate moved significantly into restrictive territory, This contrast with the ECB which has more ground to cover judging by the fact that real policy rate is still below natural rate of interest. Nevertheless, there is usually high uncertainty regarding these estimates of natural rate of interest and the this finding should be treated with cautions. All these considerations related to monetary policy orientation were addressed previously.

Third, the rising share of services in economic activity and employment which account for at least 70 percent in developed economies. Again, a higher share of services affects monetary policy transmission because services are less capital intensive and therefore less sensitive to changes in interest rates.

3. Where are the boundaries between price stability and financial stability and is there a breaking point that tilts the balance between costs and benefits of monetary policy actions?

The reality is not black or white as theory suggests… The modal view among both academics and policy makers is that price stability should be the sole goal for monetary policy, which is ill suited to target financial stability. This dogma is backed by the well known Tinbergen principle which postulates that the number of instruments used should be equal to the number of targets. This principle relates to the fact that there is only one policy rate and the desired level to ensure price stability may be quite different from the level desired to address or preserve financial stability.

…but encompassing a wide spectrum of nuances. The reality of the last two decades turned out to be more complex and not pictured in black or white as theory postulates, but rather encompassing a wide spectrum of nuances. Therefore, there is now at least anecdotal evidence and some consensus among practitioners (not necessarily academics) that financial stability is of paramount importance for monetary policy because it creates the environment in which monetary policy operates. In this regard, there may be instances in which financial stability considerations should be internalized in the cost benefit analysis of monetary policy decisions.

The most sudden shift in policy making in decades… Heading towards the end of 2021 the inflation narrative shifted markedly around the world and the transitory theme vanished. Interest rates futures and bond markets worldwide have been repricing for earlier rate hikes in the face of a persistent inflationary environment. At the same time, rate markets had to contend with additional challenges from balance sheet normalization. The world faced a rise in global tides of monetary policy normalization at a speed and magnitude that were inconceivable not long before.

...and higher for longer approach. Today, after almost two years of battling price pressures, the progress of disinflation looks unconceivably slow for many central banks. The persistency of core inflation makes many policy makers eager to hike further and remain higher for longer and to deliberately endorse an overtightening approach to restore price stability as soon as possible (at all costs). While headline consumer indices have fallen, central bankers cite higher core inflation, tight labor markets and robust the services sector as evidence that prices will continue to soar for some time yet. As a result, the tightening cycle should go further and turn even more restrictive.

Close to crossing the Rubicon… i.e. testing the boundaries between prince stability and financial stability. Of course, restoring price stability and preserving the hard won credibility is of paramount importance for central banks. While the destination is clear, there are many alternative journeys. Choosing the right journey will preserve the central banks’ credibility in the years to come.

I argue that there is currently a large risk that some central banks are about to become inflation nutters. As a result, pushing rates to the roof to mechanically hit their inflation targets may place some central banks close to testing the boundaries between price stability and financial stability. In some jurisdiction, economies may be close to the breaking point where the marginal benefit of an additional unit of policy tightening could be marginal and tilt the balance towards the costs.

If you want to get to 2% quickly you probably will make a policy error. There are lessons that must not be forgotten by central banks and the ongoing pace of disinflationary process needs to be adequately tailored to avoid possible trade offs with financial stability over the medium and long term. Policy makers actions need to be anchored by the long term sustainability of the inflation objective and not by strictly and mechanically hitting the inflation targets which will prove a mean reverting process.

Monetary policy lags understated… I strongly believe that, for the majority of central banks, the cumulative tightening deployed by the entire portfolio of monetary policy instruments is massive and is currently understated. Moreover, this narrative coined the risk of doing too much is lower than the risk of doing too little ignore an irrefutable truth of monetary policy theory and practice : monetary policy operates with long and variable lags and the transmission patterns changes (see the previous chapter).

Patience is needed for impulses to reached destination (inflation). The unprecedented policy tightening is yet to be felt and the bulk of tightening is expected to materialize in the course of this year and thereafter as usually it takes up to 2 years for monetary policy impulses to reach the destination, namely inflation. The bottom line is that patience is highly needed for monetary policy to be fully transmitted, otherwise you have the recipe for overkilling and possibly financial instability.

Financial stability sine qua non for monetary policy. The still recent developments in UK and US serve as a proof to this statement. Aggressive policy tightening as well as constantly reappraisals of the pace and extent of policy hikes gave way to large repricing of financial assets and a sharp rise in credit spreads. Moreover, higher rates can amplify risks arising from households indebtedness. Repricing the cost of credit at significantly higher level of rates – usually after a significant lag – could squeeze cash flows and deteriorate the borrowers balance sheets.

As a result, I think that from this point onward, additional policy tightening can come with significant financial stress and financial instability will impair monetary policy and endanger the price stability objective.

Avoid stop and go…or in central banks jargon “conditional pose” which let policy expectations at the mercy of markets. Another topic that I would like to put forward is the recent approach of some central banks to favor stop and go policies. With the beginning of 2023, some central banks endorsed what is called conditional pose – justified by policy makers to reassess the influence of the monetary policy stance on economic activity. In my opinion, the benefits of holding rates and leaving policy expectations at the mercy of market participants just to reinitialize the hiking cycle shortly after are close to none. What could you possible reassess over a 1 -3 months window when you are well aware that 3 months is nothing relative to the usual monetary policy transmission horizon. It may be true that you could be able to reassess the pace of policy rates (the magnitude of rate changes), but if you postulates that you are able to reassess the strategic orientation of monetary policy in 3 months window then you are meaningfully behind the curve and you fully revel that to the market.

Inflation is the ethos of monetary policy but sometimes financial stability may takes precedence. I am not postulating that central banks should abandon their ethos of price stability. Central banks should never lose sight of their commitment to price stability and should deliver their mandate. I am postulating that there could be instances when central banks may need to alter their reaction function to account for financial stability considerations. As a result, there could be episodes when financial stability should take precedence and central banks could widen their horizon and tolerate a somewhat slower return to the inflation target to avoid systemic events.