Over the past few days, we have witnessed intense debates around the topic of the “technical recession”, where various causes and accountabilities have also been circulated. Therefore, it remains to be clarified how serious it is that it is called “recession” and how severe its “technical” nature is. At the same time, it is important to understand when the current economic downturn began.

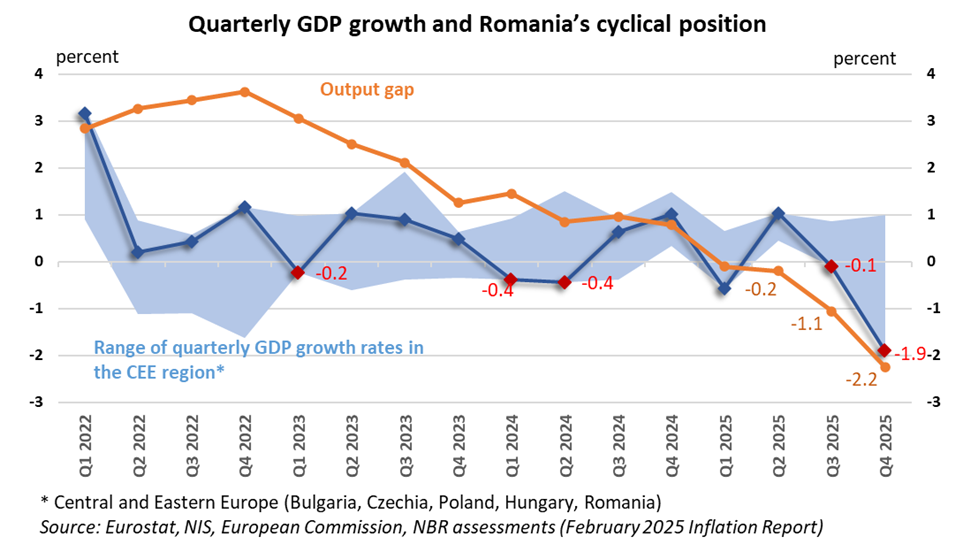

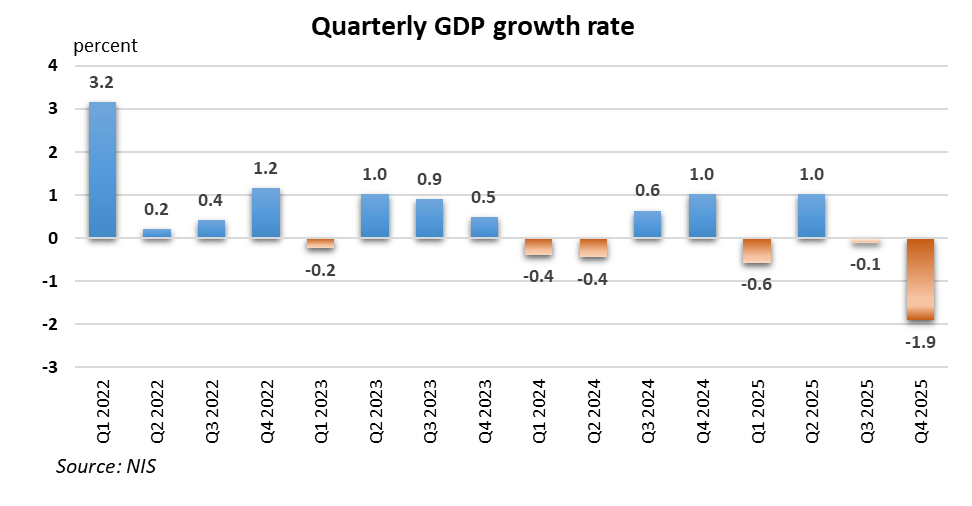

The textbook defines technical recession as two consecutive quarters of economic decline, measured by quarter-on-quarter GDP dynamics. Hence, the GDP rates of change in 2025 Q3 and Q4, i.e. -0.1% and -1.9% respectively, show Romania’s economy to be a “classic” case of technical recession.

There is a significant difference in this respect between two consecutive quarters with GDP negative growth and an overall economic recession, which reflects in the annual dynamics of domestic economies in a deep and lasting manner. However, there are also some opinions that a technical recession is, in fact, the regular forerunner of economic recession. Nevertheless, extensive empirical evidence invalidates such assumed correlations.

Romania’s case is not unique in the European Union. Ten other Member States (Denmark, Germany, Estonia, Latvia, Luxembourg, the Netherlands, Austria, Hungary, and, more recently, Finland and Ireland) have gone through episodes of technical recession over the past three years. Among these, only Germany, Austria, and Estonia recorded deep economic recessions, with two consecutive years of real GDP contraction, mainly due to shocks associated with the energy crisis caused by the outbreak of the war in Ukraine.

The technical recession should not have come as a surprise

As early as a year ago, the NBR brought attention to domestic demand slowing down sharply and the economic growth rate falling below its potential, as a result of the changes in the fiscal and income policy stance to restore the fiscal position. The prospect of a technical recession was included in the forecast scenarios already at the end of 2025.

These developments emerged after the subdued economic performance in 2024, given the weak external demand and the weather conditions that dampened the contribution of the agricultural sector to the GDP. Despite supporting domestic consumption, the strongly expansionary fiscal measures of 2024 led to the worsening of the external deficit, as excess demand was largely covered by imports.

The slippage of the fiscal deficit and the deterioration of the external balance rendered the consolidation of public finances more urgent. Fiscal adjustment measures became imperative to ensure macroeconomic stability and mitigate the vulnerabilities of the economy to external shocks, in a context in which Romania is faced with a sharp increase in public debt financing needs.

GDP estimates have been revised as of December 2025, with negative values expected for Q4, when the economic decline (-1.9%) compared to Q3 proved to be much more severe than even the rigorous forecasts. Mention should be made that most indicators correlated with GDP developments, such as the volume of trade turnover, industrial output or real wage, were already signalling a contraction trend in economic activity.

In 2025, Romania remained on the downturn of the business cycle

In 2025, the downward phase of the business cycle steepened, in a European environment broadly marked by subdued economic developments. For the fourth quarter of 2025, GDP growth in the EU was estimated at merely 0.3%, ranging relatively widely across Member States, from -1.9% for Romania, followed by -0.6% for Ireland, to 1.7% for Lithuania. In addition, some regional peers, such as Hungary and Czechia, posted modest paces of increase of below 0.5%, whereas Poland’s economy expanded by 1%, according to the flash estimates.

The business cycle shows the alternation of upturns, with output expansions above the economy’s sustainable potential, and downturns, with economic stagnation or contraction. In the latter phase, households calibrate spending more carefully, given the squeeze in their real income, the degree of uncertainty and their weaker expectations of individual financial situation. Companies become more selective with respect to investment projects and exercise a tighter control of business expenditure. Job creation decreases, and so does the capacity utilisation rate.

A key indicator for assessing the cyclical position of an economy is the output gap. Data on Romania’s quarterly growth and cyclical position show that the output gap has been following a downward trend as early as 2024. Subsequently, the demand deficit widened throughout 2025. These developments mirror the decline in household consumption, primarily in the latter half of 2025, a natural response to fiscal adjustment measures and the still tight financial conditions.

Labour market developments contributed to the downward revision of expectations regarding the general economic situation, individual financial standing and job stability. Such expectations underpinned prudent consumption and saving behaviours. The unemployment rate is nearing its highest level over the past years and the number of job vacancies is falling to a level comparable to that in the cyclical adjustment period in 2010-2012.

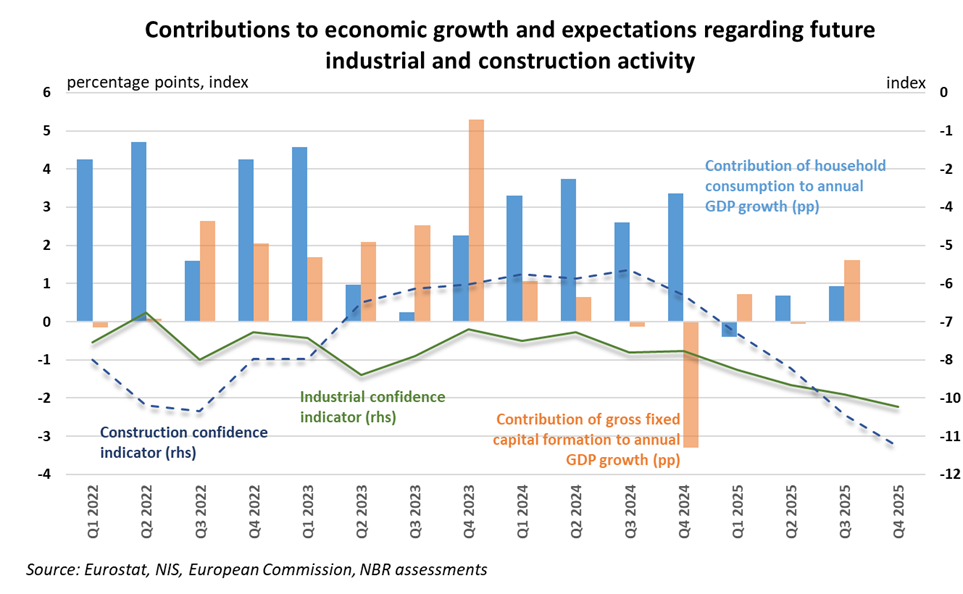

Even though economic growth has been modest already since the beginning of 2025, this year may be deemed important in terms of the needed shift of growth drivers. The sustainable change in the growth pattern means the transition from primarily consumption- to mainly investment-led growth, as shown by the chart above. Both investment in machinery, equipment and transport equipment and new construction works posted favourable growth rates.

These developments were also supported by the equipment loans extended by banks to firms, whose share exceeded 30% of total loans at end-2025, rising from approximately 27% in December 2024. It should be underlined that EU-funded investment projects bolster long-term economic growth through increasing competitiveness and stimulating private investments (crowding-in effects).

The economic downturn has become visible since 2024

The slowdown in economic growth became visibly more pronounced in 2024, when Romania’s economic activity contracted by 0.4% in two consecutive quarters, according to the recent revision of the statistical data series. These revised data would now indicate, from an ex-post perspective, a technical recession as well. In fact, the modest performance (+0.9%) in 2024 reflects the downward phase of the business cycle.

The economic downturn, in both quarterly and annual terms, occurred despite an unprecedented fiscal stimulus in the post-pandemic period. This reflected in the record-high ESA deficit of 9.3% of GDP, with the discretionary increase in deficit being mainly consumption driven. However, this unprecedented fiscal effort did not yield any results in terms of economic growth, but rather led to the build-up of burdensome macroeconomic imbalances (“twin deficits”).

The substantial budget expenditure increases in 2024 fuelled the consumption of households and general government alike, which posted in both cases strong annual growth rates of approximately 5%.

However, although consumption made a 3.2 percentage point contribution to the GDP dynamics, the net effect on economic growth was limited. The rise in domestic demand entailed the expansion of imports, and the result was a modest pace of economic advance, i.e. 0.9%. In fact, the pick-up in consumption in Romania supported the increase in production in other countries that accommodated Romanians’ large demand for imports of consumer goods and services.

Therefore, domestic production must be a key priority for Romania. For example, the industrial output volume recorded successive declines in 2023 and 2024 (-3% and -1.6% respectively), and this trend continued into 2025 as well (-0.9%). Competitiveness losses and the hike in domestic supply costs led to a sharper contraction in output and hindered the recovery of industrial activity. However, in 2025 Q3, the results in industry were relatively promising.

In 2025, in the context of inherent fiscal adjustments, the economic downturn continued to deepen, especially in terms of consumption. Specifically, consumption decreased as early as the first quarter, even before the adoption of fiscal adjustment measures. Consumption is the factor whose contraction translates directly and rapidly into the GDP dynamics, hence the negative impact on growth in Q1 (-0.6%).

The priority of strengthening public finances

Any comprehensive fiscal adjustment takes its toll on economic growth. During a year of major corrections in terms of public finances, as was the case with 2025, it was foreseeable for the pace of economic growth to slow.

However, the economy picked up in 2025 at a not-at-all-shabby rate, considering the scale of the fiscal consolidation measures implemented. The 0.6% economic advance is not a far cry from that recorded in 2024, when the economy grew by 0.9%, despite a fiscal expansion that seemed to revive the wage-led growth-type illusions.

The economy has remained in the modest performance zone, but it is noteworthy that behind this growth stood primarily investments and structural factors.

Against this background, various opinions have been expressed lamenting about the technical recession and going as far as questioning even the need for fiscal adjustment, an extreme, impossible to imagine scenario. Even in the absence of adjustment measures, Romania’s economy would not have been full steam ahead in 2025, as in the past, just like it wasn’t in 2024 either!

But there is no alternative to the need for fiscal consolidation. The consequence would be a sovereign rating with drastic, incalculable implications for economic and financial stability.

Hence, the first step in an earnest discussion is to understand Romania’s imperative to strengthen its public finances. No economy can grow soundly on the back of severe budget deficits, which mask achievements and postpone costs. And the soaring public debt ends up costing dearly and calls for painful corrections.

We need to pursue the consolidation of public finances, yet in a balanced manner, safeguarding as much as possible a certain social cohesion, as well as the political consensus required in fragile times like these, dominated by multiple external, economic and security challenges.

At the same time, the support of factors underlying economic growth is particularly important in order for the economy to return to positive territory. The adjustment efforts will be all the more sustainable as the economy steps up its annual pace of growth. Otherwise, in the absence of sturdier economic growth, the public deficit remains a burden.

The somewhat accommodative, wait-and-see stance of monetary policy can also be interpreted, to a certain extent, from the perspective of economic growth. Specifically, the monetary policy rate was kept on hold throughout 2025, amid the rekindling of inflation, yet via fiscal-administrative channels. The finetuning referred to that restrictive nature of monetary conditions aimed at striking an optimal balance between pursuing the disinflation objective and safeguarding economic growth.

Fiscal policy cannot afford more serious accommodation finetunes anytime soon. The measures so far ensure the return of budget consolidation onto the correct path, but it is important for them to be backed up by structural reforms and competitiveness-focused policies.

In 2026, the efforts to support the entrepreneurial environment and to attract major investments in the economy require adaptation to the vulnerable context, but also a prudent dosage.

There are inherent risks for the negative dynamics to extend beyond the two quarters of “technical recession”. That is precisely why the political stability in governing the country and the investor confidence are key priorities for economic recovery.

The budget for 2026, though belated, is a test of economic maturity. Reforms and adjustments managed in a balanced and responsible manner will strengthen investor and financial market confidence, and the economy will be able to return to sounder bases.

By accessing European funds, especially through the National Recovery and Resilience Plan, Romania is implementing the most important reform programme that it has committed itself to since joining the European Union.

2026 must be the year of European funds for Romania’s development!