With or without a lasting ceasefire, the Middle East war is fuelling severe uncertainties, entailing a pick-up in inflation, in tandem with a slowdown of economic activity. Over the short term, the impact on inflation stems directly from higher fuel prices. Yet long-term effects are much more difficult to project, since they hinge both on the duration and intensity of the conflict and on the pass-through to consumer prices.

The current energy situation is precisely the type of exogenous shock, without monetary causes, which central banks should, in theory, “see past it” at least for now. It is particularly important, however, both to formulate risk scenarios associated with the forecasts and to effectively communicate the monetary policy approaches.

The current context is, in fact, complicated, given the fragile fiscal situation and the recent political instability, both of which also leave their mark on monetary policy as well.

Near-Term Implications and Revision of Forecast Scenarios

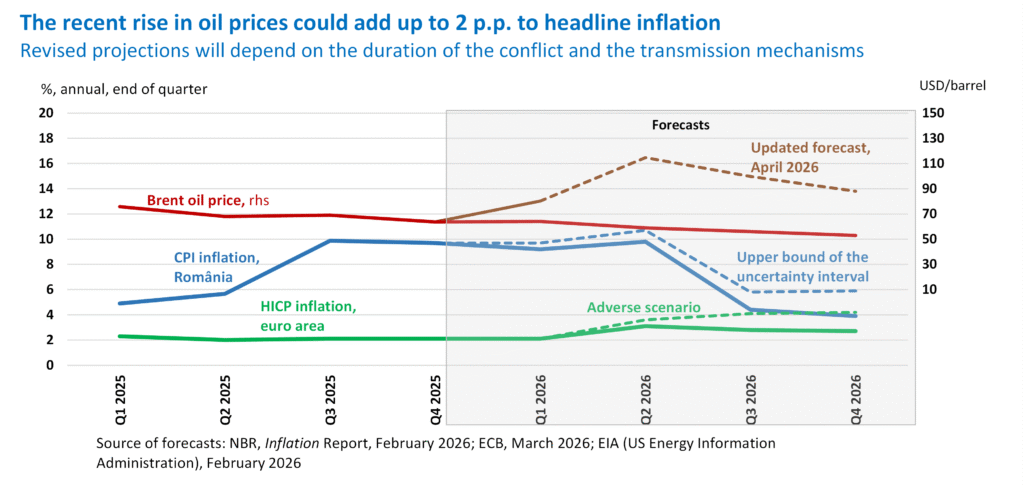

The (Brent) oil price in March, USD 103/barrel, stood on average around 50% higher than that recorded in the first two months of the year, while in April it grew to about USD 115/barrel. The EIA forecast for Q2 sees the oil price at over USD 110/barrel.

Consumer prices are hit by this shock almost instantly and even in advance, especially via the fuel price channel. However, the risk of a longer-term acceleration is higher for production costs, which will further put pressure on consumer prices.

According to the chart above, for the end of this year we can estimate increases of

1.5 to 2 percentage points – the “Hormuz inflation” – above the inflation paths projected in the absence of the Gulf shock, yet the risk spectrum actually runs much wider.

The war is already causing major disruptions to supply chains, with European producers reporting the longest delays in delivery times in almost four years. Survey indicators capture this deterioration: for instance, the euro area Purchasing Managers’ Index (PMI) for economic activity fell to 50.7 in March and to 48.6 in April, below the threshold separating expansion from a potential contraction in economic activity.

Turning to Romania, despite the negative output gap, the increase in energy prices pushed inflation to almost 10% in March, above expectations. The roughly 13% rise in fuel prices was the main culprit, while April will see a further step-up in inflation, to over 10%. Inflation has been affecting the already depressed consumption: retail sales were already down in February by 6.8% year on year.

The outlook for the coming months is not encouraging, with oil tanker traffic in the Persian Gulf still obstructed. If tensions linger, high energy prices could, via second-round effects, force the persistence of the “Hormuz inflation” over several quarters. Some relief comes, however, from the cap of the acquisition price of domestically-produced natural gas for household consumers.

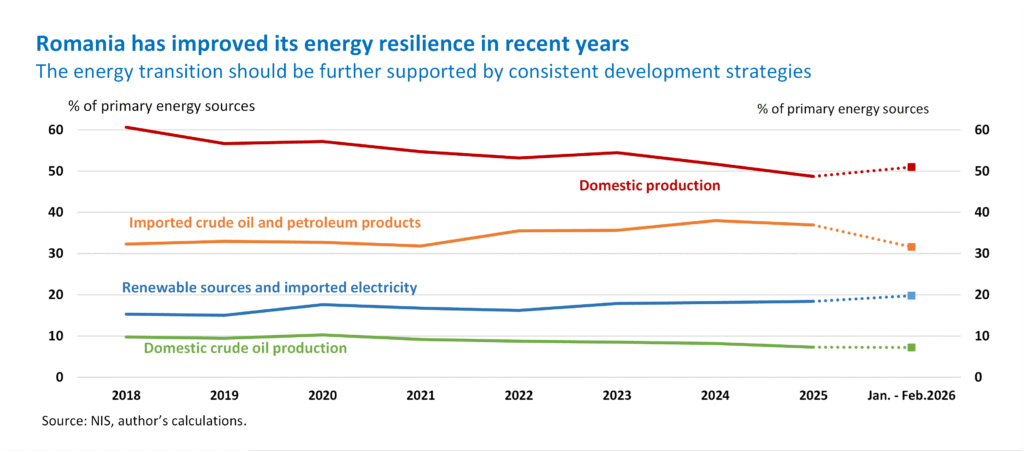

Romania’s energy dependence is lower compared to most European countries. Yet the current situation underlines the need to further reduce the reliance on fossil fuels. As shown in the chart above, imported oil makes up only one third of the primary energy resources.

How (and Whether) Central Banks Respond to “Hormuz Inflation”

The nature of the shock, the economic environment and the balance of risks prompted the NBR Board to adopt an actually anticipated wait-and-see approach at its April meeting. Yet the NBR’s response needs to be seen in a broader context.

The war triggered a surge in crude oil prices, leading to a swift rise in inflation worldwide and fuelling risks. The textbook response of central banks was to avoid changing the monetary policy parameters. This stance may change if incoming evidence points to an intensification of the energy shock and a flare-up of inflation expectations.

The sequence of crises over the past years has brought about a certain capacity of structural change in inflation expectations. And now, when the globalised trade system is fractured by tariff wars, the situation is turning even more tense. While the immediate response of central banks (ECB, Fed, Bank of England) was to preserve monetary conditions, playing it by the book, the next steps might deviate from this framework. There seems to be a certain consensus on the need for concrete actions, if the Strait of Hormuz is not reopened to normal traffic any time soon.

Inflationary risks are significant, at least over the short term, and additional pressures, in the long run, stem from the fragmentation of supply chains, limiting the supply of commodities. The tension could, however, be soothed to a certain extent through alternative transit routes, which would enable countries with overproduction to increase exports.

In parallel with inflationary pressures, negative influences are emerging in terms of economic growth prospects. The Gulf conflict is conducive to a slowdown of the world economy, pushing it at least 0.3 percentage points below the previous two years’ average (3.4%), according to IMF estimates.

At a regional level, the new energy shock overlaps with the uncertainties generated by the conflict in Ukraine. For instance, in the case of Romania, World Bank and IMF forecasts have been revised significantly downwards (by 0.7 percentage points), to 0.5% and 0.7% respectively. Under the circumstances, the NBR remained prudent in terms of forecasts, considering inter alia the persistent effects of the end-2025 “technical recession”.

The central banks’ messages and actions are calibrated to scenarios that depend on the persistence of geopolitical tensions in the Gulf. The strongly inflationary scenarios signal the need for raising policy rates, a prospect that would slow down economic activity even more. The messages built around the firm commitment to achieve the inflation target help better anchor inflation expectations, without the central bank having to pull swiftly the monetary policy levers.

An intervention now, via the tightening of monetary conditions, might prove premature from the perspective of synchronising effects in the economy, in the event that the conflict ceases relatively soon and oil tankers resume their route through the Strait of Hormuz.

And this is because monetary policy effects, visible with a certain lag, can overlap, in a contradictory manner, precisely with the easing of inflationary pressures. Moreover, the deterioration of economic growth prospects would become even more severe if central banks resorted directly to policy rate increases.

The surge in global prices is not, at present, an effect of procyclical economic policies or of the functioning of the economy per se, but has exogenous causes, with a limited timespan however. Thus, at the current juncture, the challenge would be to avoid pushing monetary policy into a risky experiment of volatility, with zigzag responses that would affect even more the predictability of economic conditions.

The decisions to raise the policy rate, as a mechanical response to the “Hormuz inflation” pressures, might prove harmful to the economy, but also to monetary policy credibility. The same goes for monetary policy easing, as a mechanical response to a decline in inflation, if disinflation does not consolidate enough over time.

Romania’s Priorities – Financial Sustainability and Economic Growth

Romania’s priority remains fiscal consolidation, not only for macroeconomic stability purposes, but also to provide the necessary room for monetary policy, given the persistence of fiscal dominance in the economic policy mix over the past years.

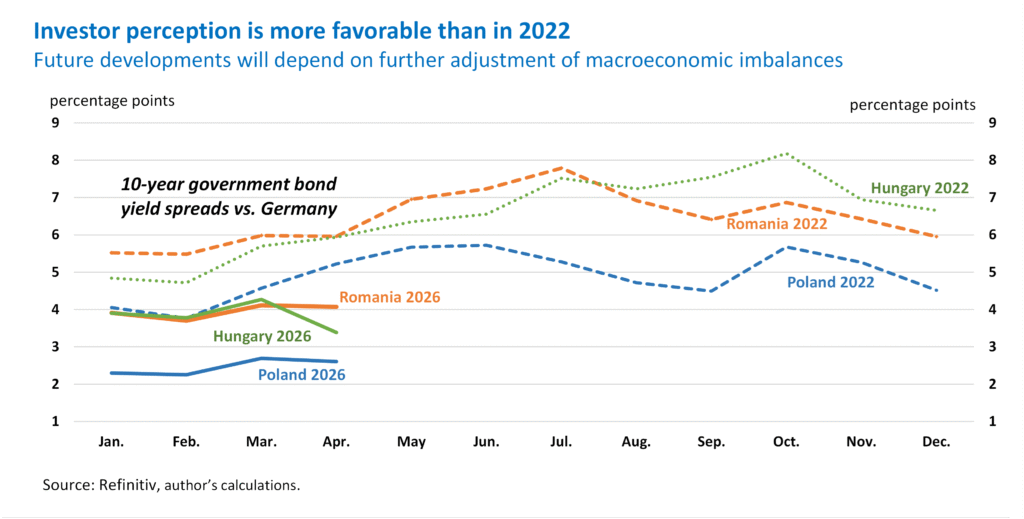

At present, Romania stands out due to high inflation and subdued economic growth, as well as for persistent budget and current account imbalances. This is reflected in investor perception, with Romania being assigned the highest risk premium in the region.

Financing costs remain a key factor for sustainable development. In the current context, however, we must point out the recent progress made by Romania and the other countries in the region, which has been reflected in a decline in risks perceived by investors.

The chart above shows that, in 2022, each of the countries shown were perceived as facing a more complex long-term risk profile than implied by the current economic risk assessments.

For Romania, the implications for the situation of public finances are particularly relevant. In 2025, interest payments on public debt amounted to 2.8% of GDP (ESA), almost twice the level recorded four years earlier, while under the 2026 budget, interest expenditure is projected to reach 3% of GDP.

For monetary policy, it has been a long time since we faced only the standard cyclical fluctuations. To remain the “guardians of stability”, central banks must assume both fine-tuning roles and hard discipline functions, to strengthen the necessary economic resilience. Ensuring price stability may at times require central banks to counterbalance unsustainable fiscal policies that threaten financial and macroeconomic stability.

In retrospect, against the backdrop of disinflation in 2024, the monetary policy rate cuts coincided with a strongly expansionary budgetary context, at the time when the fiscal policy was already “adding fuel to the fire” through higher discretionary spending.

It was therefore foreseeable that the downward trajectory of inflation recorded in 2024 would not continue throughout 2025, given the inflationary effects of budget expansion, as well as the fiscal adjustment measures required to reduce the budget deficit over the coming years, in line with Romania’s National Medium-Term Fiscal-Structural Plan, drafted and adopted in 2024.

In the current fiscal and budgetary context, when the economy is absorbing the full effects of the budget deficit adjustment measures and the negative output gap is widening to severe levels, monetary policy is faced with the challenge of avoiding “rubbing salt into the wound” by raising the key interest rate in response to the first supply-side shocks.

Despite the upward revision of the inflation path for the coming months, amid the fallout from the Gulf conflict, in April 2026, the NBR once again decided to keep the monetary policy rate unchanged. We expect the inflation rate to roughly halve during the summer months, owing to a base effect associated with the fiscal measures adopted in the summer of 2025. The decline is expected to be accompanied by the easing of core inflation, driven by the sharp loss of momentum in consumption and aggregate demand.

Thus, the conditional wait-and-see approach taken so far by the NBR is likely to continue for some time, even though other central banks could decide to act. Given the current monetary conditions and the disinflation projections, the NBR’s stance is relatively well-positioned to navigate the current uncertainties.

As regards economic policies, preventing a protracted recession in the coming period requires measures to support potential output. The efficient and timely implementation of investment projects is therefore essential.

Moreover, as pointed out in the recent report OECD Economic Surveys: Romania 2026, competitiveness and higher labour market participation are key structural objectives. Advancing the reforms needed to improve the absorption of EU funds supports the transition towards a more competitive growth model, aligned with the latest technological developments.

Romania is currently navigating a challenging period, marked by domestic political instability and volatility in the foreign exchange market as well. The depreciation of the leu has mixed effects on financial conditions in the economy. On the one hand, exporters may benefit from the decline in competitiveness deficit associated with the overvaluation of the real effective exchange rate. On the other hand, foreign currency borrowing, including by the government, becomes more expensive, while imported inflation becomes more visible.

Therefore, both external and domestic economic conditions have become considerably more challenging. Nevertheless, Romania should remain firmly anchored to the budget consolidation path, safeguard the sustainability of public finances, and continue the major investments that support the economy’s growth potential, thereby strengthening the economic resilience.

In the whirlwind of global uncertainty, the domestic political situation is undermining Romania’s economic credibility, weakening the confidence of investors and financial markets. The current political crisis is an additional headwind in an already deteriorated macroeconomic environment.

The need for political and governmental stability is particularly important this year, given the strategic importance of the objectives already committed to: strengthening public finances, implementing investment projects financed from EU funds, especially those under the NRRP, and advancing major international cooperation projects, such as joining the OECD in 2026.